Last Updated on June 12, 2023 by Parentology

Contents

Something that almost all Singaporean couples can relate to is knowing that the next big step in a relationship is when your significant other asks if you would like to apply for a BTO together. It is a decisive and bold statement, marking the love and affirmation that this person sees you in their future.

For couples who are both full-time students, this task may seem daunting. After all, the majority of students do not have full-time jobs or incomes on the side. In this article, we intend to simplify the process for you and at the same time, maximise your savings. Here is what you need to know about BTO if you are applying as a student.

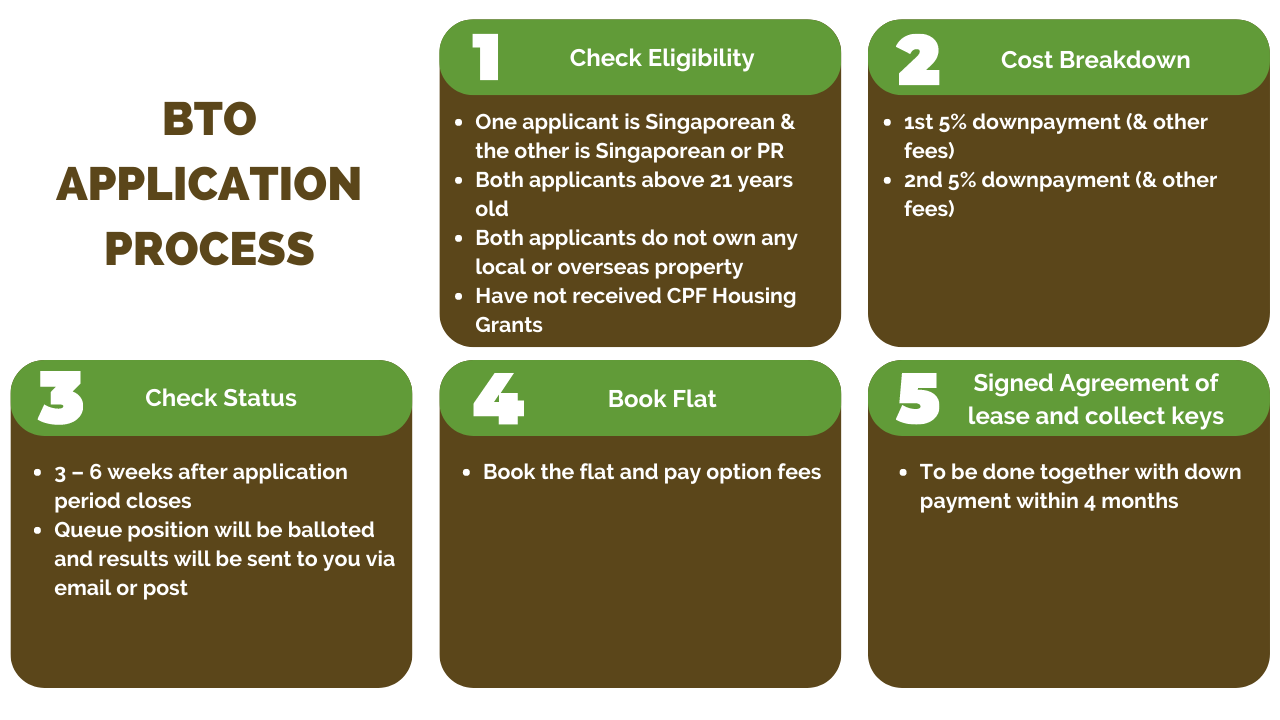

General Steps to apply for BTO

Before applying for a BTO, it is important to check your eligibility, since this is not a one-step procedure that takes time. For easier reference, we have provided a brief overview of the specific milestones and cost breakdown before moving on to the next step.

Also, with the consideration of discussing the cost of your BTO flat and how to finance it, you may want to consider the perks of HDB loans and relevant grants.

Eligibility for HDB Loans & Grants

Deferred Income Assessment

To be eligible for CPF Housing Grants and obtain an HDB housing loan as a student, the Deferred Income Assessment comes into play.

Generally, to be eligible for CPF Housing Grants and housing loans requires one of you to be employed continuously between 3-12 months:

|

Loan |

Criteria |

|

CPF Housing Grant |

You or your spouse/ fiancé(e) must have worked continuously for 12 months before applying for the flat |

| HDB Loan |

Be in continuous employment between 3 – 6 months (depending on the type of income you’ve earned) |

However, with the Deferred Income Assessment, student couples between 21-30 years old, like yourselves, can apply for your flat first, because your income will only be assessed around 3 months before their flat is completed. This helps to ensure that you do not delay your flat application. Do note that this only applies to uncompleted flats. If you are applying for a completed flat, your income will still be assessed during the flat booking appointment.

It is crucial to gather your documents for deferment of income assessment.

For full-time students, you will need a letter from the school stating your period of study and specifying if it’s full- or part-time. For full-time students who are receiving a salary working for the school (teaching or research), you’ll need a copy of the contract stating your scope of work and the conditions of the stipend. (Allowances from scholarships do not count.) A paying side hustle/part-time job outside of school doesn’t count to HDB and you won’t have to provide any documentation for this. Remember to bring these when booking your flat.

Enhanced CPF Housing Grant (EHG

A grant that you may be eligible for is the Enhanced CPF Housing Grant (EHG). This grant is meant to help all local lower – to middle–class couples afford a home. To be eligible Singaporean couples must earn $9,000 or less per month, calculated as average household income across the past 12 months. At least one applicant has to be working for at least a year. The size of the grant ranges from $5,000 to $80,000, where the grant amount is inversely proportional to your household income.

Proximity Housing Grant (PHG

A perk staying close to your parents, specifically within 4km of them can allow you to qualify for this grant. This grant can be stacked with the EHG Grant which stretches your dollar when it comes to purchasing your home. The best part is that there is no income ceiling. The grant amount is $20,000 if you live within a 4km radius of your parents/ married children. Or get $30,000 if you apply to live together as an extended family.

Staggered Downpayment Scheme

Being full-time students, it is highly likely you will be eligible for the Staggered Downpayment scheme. The first major expense you face will be the down payment which makes up 10% of the flat’s purchase price. This five-figure sum can be hard to save up for especially if you don’t have a lot of cash or money in your CPF savings yet. Here’s where the Staggered Downpayment Scheme comes into play as it allows couples under 30 years old to split their down payment into two – the first payable upon signing the lease agreement, and the second payment upon collection of their keys. This means you get to pay the first 5% after flat booking, then the next 5% when you collect your keys.

Cost Breakdown

Considering purchasing a BTO flat as a student would probably be the largest investment in your life to date. It is crucial that you understand that a big-ticket item like this could take at least a few years or even a decade to finance. What we have done is provide a brief breakdown of the different costs involved from beginning to end. In this case study, we are assuming the house you are purchasing is a 4-room HDB flat that costs $390,000.

The table also highlights savings perks to take note of throughout the process:

|

Stage |

Payment Due | $390,000 4-room Flat |

|

Submitting your application |

Application Fee (Fixed) | $10 |

| Booking your flat | Option Fee |

$2,000 |

| Signing of agreement for lease

(approx. 4 mths after flat booking) |

1st 5% Down Payment

Stamp Duty Caveat Fee (Fixed) Conveyancing Fee Minus Option Fee |

$19,500

$6,300 $64.45 $246.60 -$2,000 |

|

Total = $24,111.05 |

|

|

| Collection of keys | 2nd 5% Down Payment

Survey Fee Registration Fee (Fixed) Home Protection Scheme Fire Insurance Balance of the Purchase Price |

$19,500 $275 $38.30 $178.66 $5.50 (5 yrs) Paid via HDB loan |

| Total = $19,997.46 |

|

The unfortunate case of a breakup

No one wants this to happen, but as we all say, we don’t know what the future holds. A prudent couple would want to know what exactly are the financial repercussions and the cost of the breakup.

The cost depends on which stage of the BTO application process the couple is in, but long story short, it is costlier to break up later in the application process.

Breaking up before booking a flat won’t have any huge financial penalties, but you will be considered as having rejected a flat. Doing so more than once will have your first-timer priority suspended for one year.

Those who break up before signing the Agreement of Lease will have your option fee forfeited, and be barred from applying for and being considered an essential occupier or other HDB flats for one year.

If the agreement is signed, you will need to forfeit 5% of the purchase price of your flat, as well as your down payment, paid stamp duty, and legal fees; and also be barred from applying for other HDB flats for one year.

What To Do Next?

Just like Financial Planning, there is no doubt that buying a home is a big responsibility. Just like a committed relationship, you should be in it for the long haul.

If you and your significant other have weighed the pros and cons and are ready to take this big step but are worried about the cost, know that it is natural to be. Alternatives like borrowing from your parents (and making sure to pay them back later) or obtaining a partial loan are advised.

Feel free to get in touch with us and our professional Financial Advisor will get in touch with you to help plan your finances, should you be concerned in the next milestone in your life.

The pressures of reality is real and although you see many of your peers taking this next step, everyone is going at their own pace, so take your time to decide if it is the right decision for both of you!