Last Updated on March 14, 2022 by Parentology

NTUC Income’s new endowment savings plan, the Gro Saver Flex, is a hybrid of the usual limited pay savings plan (choice of a fixed premium term and matures in another few years) and legacy endowment plan. It retains the good feature of the Secondary Life Insured (SLI) so that you can add on the legacy building element for those that would like a long term wealth growth instrument.

One of the new savings plan from NTUC Income, it provides a single premium or limited pay premium term with accumulation period of 5 more years as well as a new policy term of until 120 years old. There are also Death, Total Permanent Disability (TPD) and Terminal Illness coverage, as well as Cancer Waiver rider available.

There is no fixed cash benefit schedule to be paid out at the end of the 2nd policy year, but you can make flexible partial withdrawal. However it is not recommended to make partial withdrawal for this Gro Saver Flex as it is not even capital guaranteed upon maturity.

More on that below.

Features At a Glance for NTUC Income’s Gro Saver Flex

Cash or SRS

Have the option to use cash or Supplementary Retirement Scheme (SRS) for the premium payment for Gro Saver Flex. SRS is only available for single premium term.

Premium and Policy Terms

NTUC Income’s Gro Saver Flex can go up to age 120 for the policy term. Premiums term ranges from single premium to 5, 10, 15, 20 and the new 25 and 30 years term. The advantage is that after your premium years have stopped, your wealth in the plan will continue to grow and compound continuously until you are age 120.

Available Premium and Policy Term

|

Premium Term (Years) |

Policy Term (Years) |

| Single Premium/5 | 10, 15, 20, 25, 30 years or till age 120 |

|

10 |

15, 20, 25, 30 years or till age 120 |

|

15 |

20, 25, 30 years or till age 120 |

| 20 |

25, 30 years or till age 120 |

| 25 |

30 years or till age 120 |

|

30 |

Till age 120 |

Source: income

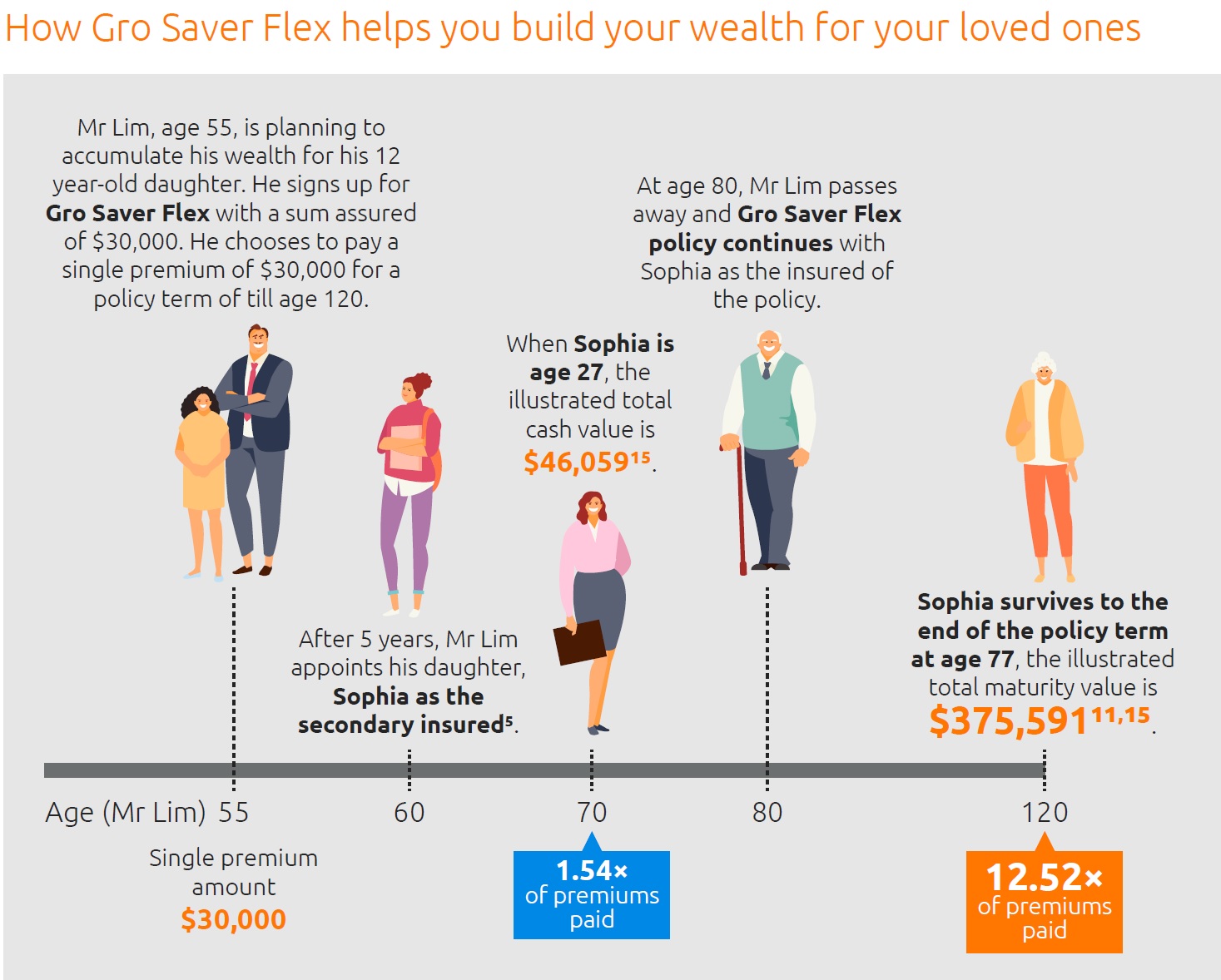

Secondary Life Insured (SLI)

Choose to appoint a spouse or child (below age 18) to continue compounding the wealth growth in the event of death of the primary life insured. The plan will continue to grow for the SLI until the original Life Insured’s 120 years old, extending the wealth growth to the next generation.

Partial Withdrawal

Withdrawal can be done fully or partially. Doing fully will terminate the whole policy.

Partial withdrawal must adhere to the minimum sum assured of $10, 000 (for single premium plans) and $25, 000 (for regular premium plans).

This means if the single premium is $10, 000 and sum assured is the same, no partial withdrawal can be done until the plan starts to generate yield and bonus.

Guaranteed Issuance Option (GIO)

Application is hassle free & simple, and acceptance is guaranteed regardless of your health condition. No medical questionnaires nor health check-up required.

Death and Terminal Illness Protection

In the event of death, family members will receive 105% of the total premiums and 101% of the surrender value (guaranteed & non guaranteed bonuses), whichever is higher, the plan will terminate thereafter paying out.

Total and Permanent Disability (TPD) Benefit

Upon TPD before age 70, this benefit pays out 2 years worth of annual premium of the base plan. With the Savings Protector Rider, it waives off future premiums of the base plan upon TPD.

Maturity Benefit

At the end of the policy term, there is a maturity amount consisting of the guaranteed and non-guaranteed yields, as well as the cash benefits of the wealth accumulated.

Retrenchment Benefit

Upon being retrenched and unemployed for consecutively 3 months, this rider will allow the policy holder not to pay the premiums for 6 months. By the 5th month if the policy holder remains retrenched, there is an option to defer the payment of premiums for another 6 months.

Guaranteed Insurability At Life Milestones

Upon reaching life’s milestones with a waiting period of 12 months after the first inception of the plan, the primary life insured can apply another life insurance coverage to protect against death and total permanent disability without undergoing medical underwriting.

Life Milestone Events Includes:

- Getting Married

- Getting First Property

- Turning 21 years old

- Having a newborn

Cancer Premium Waiver Rider (GIO)

Option to include this rider to waive off future premiums should life assured be diagnosed with advance stage cancer during premium term.

This is applicable for 1st and 3rd parties as well.

Gro Saver Flex Premium Comparison

5 years Premium Term at $30k Sum Assured

10 Years Policy Term VS Until Age 120

|

Sum Assured |

$30,000.00 | $30,000.00 |

|

Premium Term |

5 Years |

5 Years |

|

Policy Term |

10 Years | 90yo/ 120yo ALB |

| END OF POLICY YEAR / AGE |

Based on 4.25% |

Based on 4.25% |

|

Cash Value @ Year 10 |

$37,035.00 | $36,031.00 |

| Cash Value @ Year 15 | – |

$43,576.00 |

|

Cash Value @ Year 20 |

– | $53,338.00 |

| Annual Premium | $6,103.80 |

$6,103.80 |

10 years Premium Term – $3k Premium at $30k Sum Assured

15 Years Policy Term VS Until Age 120

|

Sum Assured |

$30,000.00 | $30,000.00 |

|

Premium Term |

10 Years | 10 Years |

| Policy Term | 15 Years |

90yo/ 120yo ALB |

| END OF POLICY YEAR / AGE |

Based on 4.25% |

Based on 4.25% |

| Cash Value @ Year 10 | – | $59,418.00 |

| Cash Value @ Year 15 | $40,219.00 | $39,633.00 |

|

Cash Value @ Year 20 |

– | $48,633.00 |

| Annual Premium | $3,055.50 |

$3,055.50

|

10 years Premium Term – $6k Premium

15 Years Policy Term VS Until Age 120

|

Sum Assured |

$58,910.15 | $58,910.15 |

|

Premium Term |

10 Years | 10 Years |

|

Policy Term |

15 Years |

90yo/ 120yo ALB |

| END OF POLICY YEAR / AGE |

Based on 4.25% |

Based on 4.25% |

| Cash Value @ Year 10 |

$44,904.00 |

$44,547.00 |

|

Cash Value @ Year 15 |

$78,978.00 | $77,827.00 |

| Cash Value @ Year 20 | – |

$95,500.00 |

| Annual Premium | $6,000.00 |

$6,000.00 |

How Gro Saver Flex Works

Why We Think The NTUC Income Gro Saver Flex is Suitable For You:

- Flexible Premium Terms

- For Single Premium term, have the option to use cash or SRS (Supplementary Retirement Scheme)

- Low risk endowment instrument

- Secondary Life Insured continues the wealth accumulation in the event of death for primary life assured

- Stable wealth accumulation instrument by local insurer

- Premiums stay the same and will not fluctuate

- Ease of application, no medical underwriting

What We Don’t Like About NTUC Income Gro Saver Flex:

- Not advisable for single premium or short premium (5 or 10 years) term and chooses 120 years old maturity age especially for people at young age

- Capital is not guaranteed even at the maturity year of payout

- Partial Withdrawal is available, however this is not recommended as the plan is not even capital guaranteed upon maturity, doing partial withdrawal will further corrode the wealth growth

- There are better instruments and endowment plans by other insurers that give better returns

Conclusion for Gro Saver Flex Review

The new Gro Saver Flex falls short from the predecessor of Gro Gen Saver in terms of guaranteed cash value. While Gro Gen Saver breaks even on the 13th year and is one of the strong plans in the legacy endowment arena with flexible cash withdrawal, Gro Saver Flex is not capital guaranteed.

It is not the worst plan in the market, but there are better instruments out there in terms of wealth growth and legacy endowment plan with good returns and by stable insurers.

We hope this review helps you in understanding the pros and cons of NTUC Income’s Gro Saver Flex and gives you a better consideration if it meets your savings objectives. All endowment savings plans have their own advantages and disadvantages and it is recommended that you choose one that is within your objectives and liquidity needs to ensure you get the best possible value.

The many different functions and features of a savings plan largely depends on what your concerns and needs are. When it comes to the suitability of for you and your child, it is always advised to have a look around and compare across the different competitive insurers.

To find the most suitably plan based on your concerns and needs, simply fill in the form below and our friendly partnered licensed FA advisor will get in touch with you.

Based on your needs, a custom made solution will be adjusted only addressing your concern with no obligations nor hidden fees.

Find the most suitable coverage for you and your child today!